| The

olive production industry comprises mainly two industrial sub-sectors

-table olives and olive oil production- that are highly relevant for regional

economic growth and development in Argentina. Both activities share the

same raw material, 60% of which is used for olive oil production, with

the remainder being allocated to table olives. This ratio is a function

of several factors, including the supply of varietals and product prices

in the international marketplace.

A CHANGING SCENARIO

-

Most indicators in this

business have improved in recent years, both for table olives and

for olive oil, thus allowing Argentina to improve its market share

and its positioning as a global producer.

-

Just like a decade ago, the

European Union concentrates world production, with Spain prevailing

over other EU countries.

-

In the Americas, Argentina

ranks as the No. 1 olive producer, though the momentum the sector

(especially olive oil production) has gained in other countries such

as Chile is also worth underscoring.

-

According to interim figures

for the 2007/08 crop year released by the International Olive Oil

Council (IOOC), Argentina will account for 5% of table olive production,

and for 0.9% in the case of olive oil.

-

These figures will position

Argentina in the 7th and 10th place, respectively, in the world’s

olive production ranking.

-

The origins of this crop

in Argentina can be traced back to the Spanish conquest. The sector

went through various upturns and downturns, bur the current expansion

cycle commenced in the ‘90s, with the inflow of capitals alien

to this sector into the existing regional economies.

-

Hence, there were major improvements

in picking technologies, and new varieties were added to produce olive

oil varietals and table olives.

-

Catamarca, La Rioja and San

Juan Provinces –which make up the olive map together with Córdoba,

Mendoza and Buenos Aires– benefited the most from this economic

development. Today, expansion projects are also under way in the Provinces

of Rio Negro and San Luis, among other regions.

-

In this scenario, it is necessary

to draw attention to the differences between existing or traditional

production and the new forms that have emerged in recent years.

-

Modern plantations are characterized

by a high density, and they are subject to more sophisticated management

techniques.

-

The addition of new technologies

resulted, among other things, in an increase in estimated mean yields

from 5-6 tons /hectare to 10-12 tons / hectare (1 hectare= 2.4710

acres).

-

Several public and private

institutions work today within the scope of the Foro Nacional Olivalero

(Argentine Olive Production Forum) to encourage the streamlining of

traditional sectors with a view to meeting current market demand by

restructuring this segment to provide high value-added products and

diversifying production to meet premium quality market niches.

-

The results of this transformation

effort will become apparent in the next few years, with the ensuing

spillover effect in each region involved.

-

As to production volumes,

new plantations began to bear fruit in the early years of this decade.

-

Argentina reached a record

high in olive oil and table olive production in the 2007 crop season

with some 25,000 tons and 95,000 tons, respectively, and similar values

are forecast for the 2008 campaign, in view of some problems generated

by adverse weather conditions.

-

These figures are expected

to double in the next decade.

FOREIGN TRADE

Exports

|

| Evolution

in Table Olive Exports 2007 - 2008 |

| |

|

..Source: National

Food Administration based on provisional data

..from

Customs.

|

|

-

Table olive exports totaled

90,554 tons in 2007, with foreign currency revenues of USD 120.5 million

FOB.

-

This constitutes a 29.2%

increase in value terms and an 11.6% rise by volume vis-à-vis

2006.

-

The general average price,

with a 15.7% increase, shows the same trend.

-

These figures confirm the

continued upward trend for this product in recent years.

-

Transactions in the first

year of the series under review (2000) totaled 34,666 tons with revenues

of USD 51.2 million FOB. Cumulative variations (2007 vs. 2000) amount

to 135.5% in value terms and 161.2% by volume.

|

| Evolution

in Table Olive Exports in First 2 Month Periods Trimester 2000-

2008 |

| |

|

..Source: National

Food Administration based on provisional data

..from

Customs.

|

Source: National Food Administration

based on provisional data rom Customs. |

-

The lowest volume was recorded

in 2001 (31,844 tons), whereas the floor in terms of value was reached

in 2002 (USD 32.2 million FOB).

-

Table olives in brine account

for 87.1% in value terms and 85.2% by volume of all exports, i.e.

a 19.6% and 2.9% growth, respectively, as against figures for 2006.

-

Moreover, the general average

price of table olives in brine showed a 16.2% increase in 2007 vis-à-vis

2006 (USD 1,361 FOB vs. USD 1,171 FOB).

-

Of total exports during 2007,

12.4% by volume and 20.9% by value correspond to fractioned products.

These went down 1.2% by volume and 1.8% in value terms as against

the preceding period.

-

The general average price

for these products went up by 16.8% as compared to 2006, to a total

of USD 2,236 FOB/ton.

Table 1 - Table

Olives Exports

| |

2006 |

2007 |

Variation

2007 vs 2006 |

| |

US$ FOB |

Tons |

US$ FOB |

Tons |

Value |

Volume |

|

Table Olives in Brine |

87.791.462 |

74.958 |

104.986.316 |

77.115 |

19,9% |

2,9% |

| Others |

5.463.739 |

6.159 |

15.4196.065 |

13.439 |

183,6% |

118,5% |

| Total |

93.255.202 |

81.109 |

120.482.381 |

90.554 |

29,2% |

11,6% |

..Source: National

Food Administration based on data of Customs.

|

-

Table olives sold in bulk

increased their market share, both in volume and value terms, as they

accounted for 87.6% and 79.1%, respectively, of total exports.

-

In 2007, the general average

price was USD 1,203 FOB/ton, i.e., a 16.9% above 2006 average prices.

-

Exports were shipped to 32

destinations in 2007. Brazil ranked first, with 53,188 tons and USD

63.7 million FOB, thus continuing with the current trend.

-

The USA ranked second, with

22,319 tons (and revenues of USD 35.2 million FOB). This market accounts

for 29.2% in value terms and 24.6% by volume, and shows an increase

as against 2006.

-

Shipments to Spain went down

from 19.8% in value terms and 16.5% by volume in 2006 to 2.7% and

3.1%, respectively, in 2007.

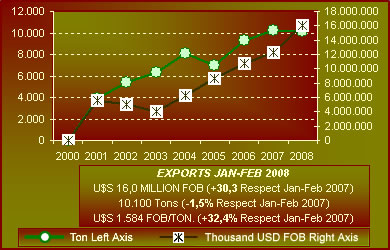

-

In the first two months of

2008, exports totaled 10,100 tons, with revenues of USD 16.0 million

FOB, i.e. a general average price of USD 1,584 FOB/ton.

-

Compared to the same period

of 2007, these figures show a 30.3% increase in value terms, a 32.4%

rise in the average price and a 1.5% decrease in the transacted volume.

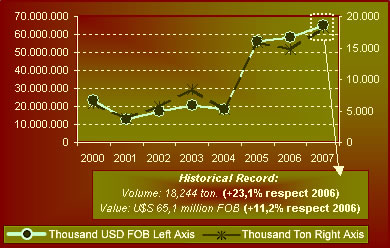

-

In turn, olive oil exports

reached a new historic record, as they grew by 23.1% by volume and

by 11.2% in value terms as compared to 2006. The export volume amounted

to 18,244 tons, with revenues of USD 65.1 million FOB.

-

This represents a 192.7%

and 181.2% increase by volume and by value, respectively, from the

sales recorded in 2000.

-

Virgin olive oil accounted

for the largest share of transactions: 91.7% by volume and 91.4% of

total export value, (+25.6% and +12.9%, respectively, vis-à-vis

2006).

-

Fractioned products accounted

for 28.8% by volume and 37.9% in value terms of total exports.

|

|

| Evolution

in Olive Oil Exports 2000 - 2007 |

| |

|

..Source: National

Food Administration based on provisional data

..from

Customs.

|

|

-

Exports grew 2.2 percentage

points in value terms, but volumes went down by an identical percentage

as compared to the preceding period.

-

The general average price

went up by 3.2% from 2006 levels, to a total of USD 4,694 FOB per

ton.

-

The market share of olive

oil sold in bulk grew by 2.2% by volume, but it went down by an identical

percentage in value terms as against 2006.

-

The general average price

was USD 3,113 FOB/ton, down by 15.4% vis-à-vis 2006.

-

Olive oil was exported to

39 countries, with the USA being the No. 1 importer –both in

terms of volume and value–, thus maintaining the trend noted

in 2006 (it accounted for 44.4% by value and 50.0% by volume of exports).

-

Brazil ranked second, with

41.7% in value terms and 35.5% by volume.

Table 2 - Olive

Oil Exports

| |

2006 |

2007 |

Variation

2007 vs 2006 |

| |

US$ FOB |

Tons |

US$

FOB |

Tons |

Value |

Volume |

| Virgin Olive Oil |

52.725.307 |

13.316 |

59.511.869 |

16.723 |

12,9% |

25,6% |

| Olive Oil |

486.238 |

121 |

269.365 |

68 |

-44,6% |

-43,8% |

Refined

Olive Oil |

5.329.776 |

1.387 |

5.313.678 |

1.453 |

0,3% |

4,7% |

| Total |

58.541.365 |

14.825 |

65.094.912 |

18.244 |

29,2% |

11,6% |

..Source: National

Food Administration based on data of Customs.

|

-

Spain went down from the

3rd to the 9th place, given that both in terms of volume and value

its share dropped from 8.0% and 8.3% to 0.7% and 0.6%, respectively.

-

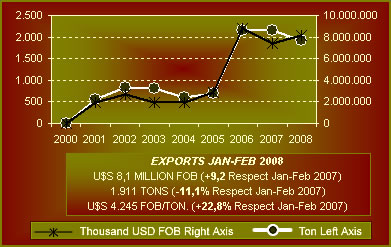

Olive oil exports totaled

1,910 tons in the first two months of 2008, with revenues of USD 8.1

million FOB.

|

| Evolution

in Olive Oil Exports in First 2 Month

Periods Trimester 2000 - 2008 |

| |

|

..Source: National

Food Administration based on provisional data

..from

Customs.

|

|

-

The general average price

was USD 4,245 FOB/ton this month.

-

These figures evidence an

average improvement of 9.2% by value and a 22.8% rise in the average

price, and an 11.1% reduction in the transacted volume compared to

the same period of 2006.

Imports

-

Table olive imports in 2007

amounted to 28 tons with a value of USD 115,890 CIF, i.e. a +17.8%

variation in value terms and -0.2% by volume as against 2006.

-

Imports came from 9 countries,

mainly Spain, Italy and China, which accounted for 92.9%, 4.0% and

2.6%, respectively.

-

As regards olive oil, the

transacted volume was 294 tons and USD 1.5 million CIF, i.e. +103.8%

and +74.4% by volume and value, respectively, from 2006 figures.

-

Imports came from 13 countries,

the No. 1 source being Tunisia (37.6% of the marketed value), followed

by Spain and Italy (28.2% and 23.9%, respectively).

|