|

|

|

|

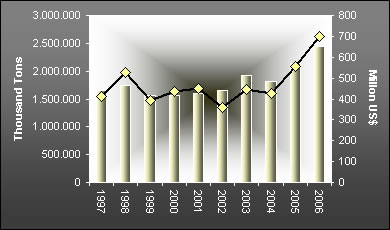

The Argentine sugar sector has shown a remarkable production increase in recent years. However, there was no need of increasing the planted area in a considerable way. While the whole area corresponding to the producing provinces (Salta, Jujuy and Tucumán) is around 250,000 hectares, the volumes obtained indicate a clear growth. The graph 1 shows the evolution of sugar production in Argentina in the last 10 years, in volume and in dollars. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

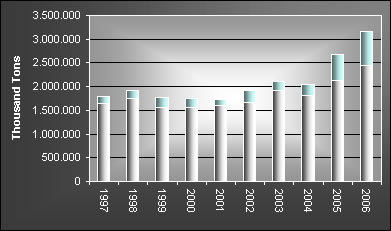

| The

sugar sector supplies mainly the local market, and is trying to

increase exports aiming at achieving higher production levels.

The results of these efforts are reflected in the chart 2, that

shows the comparative evolution of production and exports in the

last decade.

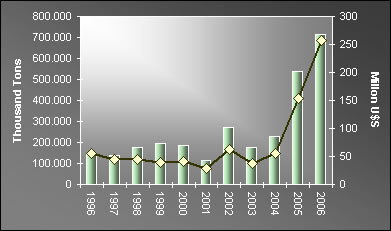

It can be observed that in recent years as production increased, there was a consequent increase in exports. 2006 production (2.4 million tons of crude sugar) was 32% higher than that of 2004 (1.8 million tons of crude sugar), and in the same period exports increased 217.20%. The graph 3 shows Argentine sugar exports in volume and in dollars for the period 1996-2006. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

These factors are to be added to the fact that in the world there are 9 million tons exceeding world demand. The result of this is a fall in the international price that is usually referred to the London Contract Nr. 5 for white sugar. The quotation reached its peak of US$ 500 in 2006. At the moment, it is around US$ 309, and in spite of having decreased it continues to be a very good price.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |