| Few

sectors in the domestic food and beverage industry are as dynamic as the

yogurt and fermented milk segment. On-going differentiation strategies

and the launching of products adapted to increasingly specific consumer

demands are based on strong R & D investment, underpinned by comprehensive

customer services, and substantial advertising campaigns. Argentina’s

production has undergone a 90% expansion in the last five years, and set

a historic record in 2007 – reaching 510 thousand tons. The boost

in the domestic per capita consumption was a decisive factor, as in the

same period it rose from 7kg (15.43 lb.) to nearly 13 kg (28.66 lb.)/inhab./year.

PRODUCT

-

Article 576 of the Argentine

Food Code (CAA as per its Spanish acronym) provides an overall definition

of fermented milks (a group including, among others, yogurt and fermented

milk proper) as “...products to which other food substances

may be added or not, obtained by coagulation and pH decrease in milk

or reconstituted milk, to which other dairy products may be added

or not, by lactic acid fermentation through the action of specific

microorganism cultures. These specific microorganisms shall be viable,

active, and abundant in the end product throughout its shelf life.”

-

This paper, save for the

exceptions stated below, shall refer to the yogurt and fermented milk

market as a whole, since these products are not usually segregated

in the literature and the domestic and international statistics available.

PRODUCTION

-

The main international databases

(FAO / USDA) do not have either world or by country production series

for this product, so that in this sense we only analyze the Argentine

scenario.

-

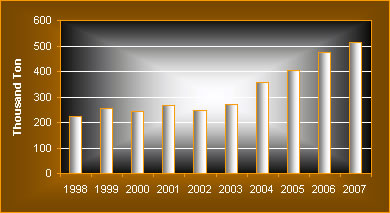

An analysis of the domestic

yogurt and fermented milk production trend in the last decade (Chart

1) identifies two well-defined stages – a first stage of continuous

albeit fairly gentle ups and downs, and a final five year-period of

great expansion, in line with the increasing consumption in the domestic

market, where these products are mostly sold.

-

In the period 2003-2007,

production rose at a cumulative annual rate of 17%, until last year,

when it broke a historic record of nearly 513,000 tons.

|

|

| Argentine

Yogurth and Fermented Milk production |

| |

|

..* Provisional data.

..Source:

Agreement S.A.G.P. y A. - CIL - FIEL.

|

|

-

This last figure shows an

8% increase as against 2006, and it is even more relevant if compared

to the performance of other high-volume manufacturing sectors. Indeed,

although these are interim figures for the January-September period,

between 2006 and 2007, production of fluid milks showed a modest 2%

improvement, while production of cheeses rose by 5%, and powdered

milk dropped by 33%.

-

If fluid milks are not included

in the analysis, in 2006 yogurt ranked for the first time as the major

product in terms of manufacturing volume in Argentina, even surpassing

the entire cheese production. The preliminary trend for the first

nine months in 2007 may lead us to believe that such leadership may

likely continue.

-

According to the latest data

available, in 2007, nearly 4.6% of the total raw milk volume processed

by the industry was used to make yogurt. Considering an average 0.79

liter/kg requirement, the volume produced accounts for 33% of all

“dairy products”, or 16% of the “milk and dairy

products” category.

-

In 2007, the gross ex factory

production value (not including VAT) was estimated at AR$1.2 billion.

RAW MATERIALS

-

The burden that the raw

milk cost has in the end shelf price (not including VAT) of this type

of products is quite variable given the wide range of presentations.

However, it may be estimated between 5% for fermented milks and up

to 25% for full-fat yogurt smoothies in 1 kg. (35.27 oz.) sachets.

-

The manufacture of these

products requires premium quality milk, with a low bacterial content

to avoid competition with the inoculated bacteria strains. No enzymes

or chemicals should be present that may hinder fermentation.

-

Industrial yields fluctuate,

among other reasons, with the type of yogurt (basically with additives),

season (due to the varying fat and protein content in fresh raw milk

and greater wastage through evaporation at high room temperatures),

with minimum levels in summer and maximum levels in winter. In 2007,

an average of 0.8 liters (27.05 oz.) of fresh raw milk was used to

obtain 1 kg (35.27 oz.) of yogurt.

CONSUMPTION

-

In the global market, the

demand for fermented milk product has good prospects as a result of

the trend to consume natural, fresh, and healthy foods.

-

Additionally, the manufacture

of “functional foods”, enriched with ingredients like

calcium or specific bacteria, is providing new differentiation opportunities.

-

Globalization brought about

the rapid incorporation of the Argentine market (one of the most developed

and interesting in Latin America) to the international trends. This

was made possible, in the particular case of fermented milk products,

through the landing, in the mid-90s, of Danone, one of the world leaders

in the sector, which partnered with La Serenísima, Argentina’s

No. 1 manufacturer.

|

|

| Per

capita Yogurt and Fermented Milk domestic consumtion |

| |

|

..Source: Agreement S.A.G.P. y A. -

CIL - FIEL.

|

|

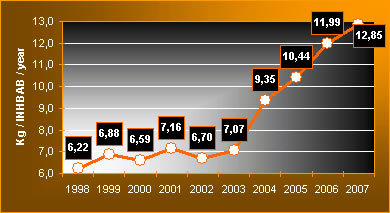

-

The first domestic consumption

boom occurred between 1990 and 1994 as a result of a significant increase

in purchasing power, strong promotion campaigns, and changes in consumer

habits. In this five-year period, the cumulative annual rate amounted

to 14%. Hence, Argentina’s average consumption rose from 4 kg

(8.81 lb.) to 7 kg (15.43 lb.)/inhab./year.

-

An analysis of consumption

trends in the last decade (See Charts 2 and 3) identifies a second

stage of remarkable expansion. After five years (1998-2002) marked

by falling income, stable or decreasing prices, and fluctuating consumption,

the sector entered a new period of steady growth, with a cumulative

annual rate of 16% in the period 2003-2007.

-

Devaluation was followed

by a strong surge in product prices, which could only be offset in

2003 with a pickup in income. This, along with the strong promotion

campaigns conducted by the leading manufacturers, spurred a boom in

consumption which went from 7 kg (15.43 lb.)/inhab./year in 2003 to

nearly 13 kg (28.66 lb.)/inhab./year as estimated for 2007 (+82% between

both values).

-

Yogurt and fermented milks

are consumed in spring-summer, with the highest levels reached in

November-December, and the lowest in May-June.

-

In recent years, seasonality

has decreased. In 2003, the difference between positive and negative

consumption peaks reached 100%, while in 2006/7 it became more stable,

at around 55%. This reduced seasonality may be explained by higher

autumn-winter relative levels and not by the recovery seen in the

last two months of the year.

DOMESTIC MARKET

-

The yogurt market is one

of the most dynamic ones in the dairy sector. Its strategy is based

on constant differentiation and the launching of new products by incorporating

additives, packaging variation and innovation, and by adapting to

new consumer demands. Also, a strong investment has been made in R&D,

customer service, and advertising.

-

Companies tend to meet the

needs of increasingly specific consumer groups by developing products

for children, youths, sports people, women, adult and elderly customers,

celiac patients, etc.

-

Products are therefore differentiated

by consistency (set, whipped, and smoothie), by fat content (with

cream, full-fat, low-fat or fat-free), and by flavor (natural or flavored).

Apart from these presentations, yogurts may include a wide range of

additives – fruit pulp or pieces, juice, cereal, cream, honey,

probiotic and symbiotic microorganisms, prebiotic ingredients, iron

sulfate, calcium, vitamins, among others.

|

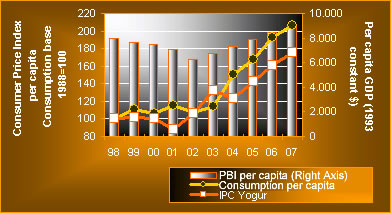

| Yogurt

consumption and it’s relation to income and price |

| |

|

..Source: Agreement S.A.G.P. y A. -

CIL - FIEL.

|

|

-

The addition of probiotic

and symbiotic microorganisms deserves a special note. In line with

the global trend, the manufacture of “functional foods”,

enriched with specific bacteria, is currently very popular in Argentina.

For instance, Danone-La Serenísima has introduced the concepts

of “Probio2”, “Biopuritas”, “Provitalis”,

or ”Acti Regularis”; Sancor, for its part, has launched

the “Biototal” concept, which combines natural ferments

selected by the manufacturer with calcium, vitamins, and minerals.

Likewise, Suc. de Alfredo Williner has introduced the BB-12 prebiotic

culture into its Ilolay Vita Bioarmonis yogurt line, which contributes

to a balanced intestinal flora.

-

Packaging differentiation

strategies are under continuous development:

-

Shapes: cups, bottles, and sachets.

- Content: 80, 95, and

100 gr. (2.82, 3.35, and 3.52 oz.) (fermented milks), 70, 125, 163,

170, 172, 175, 180, 183, 190, 195, and 200 gr. (2.82, 4.40, 5.74,

5.99, 6.06, 6.17, 6.34, 6.45, 6.70, 6.87, and 7.05 oz.) (usually,

yogurt in small plastic bottles or cups), or 700 and 1,000 gr. (24.69

and 35.27 oz.) (yogurt in sachets).

- Materials: at present different kinds of plastic

are almost exclusively used: low-density polyethylene (for sachets)

and high-density polyethylene, polystyrene, and polypropylene (for

cups and bottles). Some stores sell glass containers (only products

from the Dahi brand, an SME from Pilar, Buenos Aires Province).

-

Color is another differentiation

element used to make the product stand out on the shelves and identify

segments. At the beginning, color was limited to green on diet product

labels, but then it spread to containers. Today, the major manufacturers

identify their full-fat yogurt lines in blue and low-fat lines in

green hues.

-

Just to show the wealth of

presentations on retail shelves, it should be noted that the two leading

companies, Danone and UTE Sancor/DPA, include more than 100 different

product codes in their price lists corresponding both to yogurts and

fermented milks.

-

Given the perishable nature

of the products and the need to ensure a continuous cold chain, distribution

logistics play a key role, so only the leading companies have a national

reach.

-

Due to the wide range of

yogurt products and packaging, it is extremely difficult to estimate

an average price that may account for such diversity. Since November

2001, the National Institute of Statistics and Census (INDEC as per

its Spanish acronym) monitors the price of creamy yogurt in 200 gr.

(6.76 oz.) cups as a sample product.

-

The consumer price of this

sample product showed a stable trend from 1998-2002, and a 42% rise

from 2004-07 (See Chart 3). In March 2008, the price was AR$1.35-1.40,

i.e., AR$6.75-7.00/kg. At the time, the price of a 1-liter (33.81

oz.) sachet on the retail shelf was almost 50% cheaper.

-

With regard to fermented

milks, in March 2008, the consumer price of a 100 gr. (3.52 oz.) bottle

of classic or 0% fat Actimel, for instance, was in the range of AR$1.25

(AR$12.5/kg.), while the price of the 95 gr. (3.35 oz.) Sancor Bio

bottle was around AR$1.15 (AR$12/kg.).

FOREIGN MARKET

-

Due to their high perishability

and long-haul transportation problems, these products are almost exclusively

sold in the domestic market.

-

According to Comtrade, world

exports of yogurt and other fermented milk products grew by 90% from

2002-2006, to a total of USD 3 billion last year, of which 50% corresponds

to yogurt.

-

The major individual exporters

are Germany, France, and Belgium, which together account for nearly

53% of the total volume.

-

In Argentina, the “yogurts

and other fermented milk products” sector is one of the few

negative items in the dairy products balance of trade, which at an

aggregate level has always been favorable in the last decade. Since

2005, however, the balance of trade has been positive and growing.

|

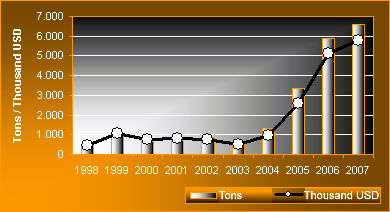

|

| Argentina

Yogurt exports |

| |

|

..* Provisional data.

..Source:

Customs & INDEC.

|

|

-

Overall, Argentine export

volumes and amounts were negligible during the period under review,

both as against domestic production and total dairy product exports.

As a matter of fact, yogurt exports accounted for a maximum 2.6% of

total dairy product volumes (in 2007), while the domestic production/export

ratio grew over 1% only in the 2006-07 two-year period.

-

Between 2003 and 2007, the

exported volumes increased tenfold, and set another historic record

last year, with 6,600 tons, which accounted for a revenue of nearly

USD6 million FOB.

-

In the last ten years, except

for year 1999, yogurt was the most exported product category, representing

an average of 67% by volume. The remainder corresponds to other fermented

milks, whose contribution to the total volume has significantly decreased,

especially in the last four years, currently reaching 18%.

-

Since 1993, when exports

started to maintain some continuity, sales went mostly to two or three

neighboring countries. In the last decade, Uruguay has been the major

importer. This country absorbed 62% of exports in 2007, followed from

a distance by Chile with 33%.

-

Imports were also negligible

in the ten year period going between 1998 and 2007, and attained their

peak in 2002, when they barely accounted for a little more than 2%

of total domestic consumption.

-

As to the share of yogurts

and other fermented milk products in total dairy imports, in 6 out

of the last 10 years, it was less than 10%, with a peak in 2002, when

the group held slightly more than half the total import volume.

Table 1

| Company |

Brand |

| Danone–La

Serenísima |

Yogurísimo,

full fat - Go, Energía Total, Cremix, among others - and Ser,

in low-fat - Libre, Fibramix, Cool, among others Activia, Actimel

- Fermented Milk. |

| UTE SanCor-DPA

Nestlé |

Yógs,

full fat and Vida, in low-fat - SanCor Bio - Fermented Milk |

| Milkaut |

Milkaut |

| Williner |

Ilolay –

Ilolay Vita - Ilolay Kids |

| Lácteos

Conosur |

La Suipachense |

| Coop. Tamb.

Gualeguaychú |

Cotagú |

| García

Hnos. |

Tregar |

| Yakult |

Yakult - Fermented

Milk Product |

| Manfrey |

Manfrey |

..Source: INTI

Quality Department. |

-

With regard to the import

structure, as from 2002, all shipments consisted of other fermented

milk products, basically Actimel and Yakult fermented milks, and today

exclusively the latter.

-

Since 2000, Brazil has become

an almost exclusive supplier.

-

In 2007, imports totaled

1,250 tons, which represented an outlay of nearly USD 1 million FOB.

-

The Extra-zone Import Duty

in place for the set of products described under Item 0403, which

includes yogurts and other fermented milk products, amounts to 16%,

while the Export Duty is 5%, and Drawbacks, both Intra and Extra-zone,

total 1.5% for products with a net content equal to or lower than

1 liter (33.81 oz.), and 1.15% for products in larger packages (Information

at March 2008).

MANUFACTURERS AND BRANDS

-

Although there is no complete

information on the universe of dairy companies in Argentina, out of

a sample of 70 dairies surveyed by the Food Industry Administration

within the framework of the SAGPyA – CIL – FIEL Agreement,

in 2007 only 20 companies manufactured yogurt or fermented milk.

-

The major companies are Danone,

which in the mid-1990s acquired 100% of the equity interests in Mastellone’s

business, Unión Transitoria de Empresa SanCor-Dairy Partners

América (Nestlé-Fonterra), Manfrey, Milkaut, Williner,

Lácteos Conosur-Suipachense, García Hnos. Agroindustrial,

La Lácteo, and Orlando y Celso Peiretti (Lácteos Ramolac).

-

In terms of market concentration

by company, it is estimated that in 2007 the first 5 companies held

nearly 90% of production, with the first 3 having slightly more than

80%.

-

The table 1 illustrates the

main yogurt and fermented milk brands sold at the major supermarket

chains in Buenos Aires city, as well as their corresponding manufacturers

(based on data gathered in March 2008):

-

During the survey conducted

at the major supermarket chains, which should be considered for illustrative

purposes only, 3 yogurt lines were identified on the shelves having

the distributor’s own brand and manufactured by about as many

dairies.

Table 2

| Company |

Brand |

Certification |

Year |

Product |

| Danone S.A |

Longchamps,

Buenos Aires Prov. |

ISO

9001:2000 |

1999 |

Yogurts, cheese

spreads & desserts

|

| Danone S.A |

Longchamps,

Buenos Aires Prov.

Córdoba city, Córdoba Prov. |

ISO

14001:2004 |

2001 |

Yogurts, fermented

milks, cheese

spreads & desserts |

| Sancor |

Bella Italia,

Sta. Fe Prov. |

HACCP |

2002 |

Yogurts, desserts,

and custards |

| Williner |

Freyre, CórdobaProv. |

ISO

9001:2000

|

2001 |

Yogurts, cream,

and ricotta

|

| Manfrey |

|

ISO

9001:2000 |

2007 |

Yogurts, among

other dairy products

|

..Source: INTI Quality Department. |

-

These are: Great Value (Wal

Mart’s own brand, with a line of set yogurts in 160 gr. (5.64

oz.) cups, manufactured by Establecimiento San Ignacio) and COTO (a

line of flavored yogurts in 200 gr. (7.05 oz.) cups, and a line of

smoothies in 1-liter (33.81 oz.) sachets, both manufactured by UTE

Sancor-DPA)

-

Although no quantitative

data is available to confirm this, in recent years the own brands

of major distribution chains have fallen behind, a trend that reached

a peak after the post-devaluation crisis. This phenomenon might be

seen as a sign of market recovery.

QUALITY CERTIFICATION

STANDARDS

-

According to the Instituto

Nacional de Tecnología Industrial (INTI) (National Institute

of Industrial Technology) database, in March 2008, the dairy sector

obtained five Quality Assurance Standard certifications on yogurt

production, as illustrated 2 above.

CONSULTED SOURCES

FAO – Comtrade database -

Guardini E. y Labriola S. Dirección de Ind. Alimentaria, SAGPyA,

2008. Dairy Products Statistics at www.alimentosargentinos.gov.ar/lacteos/default.asp

- SAGPyA-CIL-FIEL Agreement – Brochures and websites from various

dairy companies - INDEC – General Customs Administration AFIP (Federal

Administration of Public Revenue) - INTI Quality Department http://nina.inti.gov.ar/calidad/index.html

- INDEC Informa - Newspaper and Specialist Magazine Articles – Argentine

Codex Alimentarius. |