In

the period 1998-2007, the world pear production increased by 30%, while

apple production remained stable, and so did the exports of both fruits.

In 2007, the world fresh apple and fresh pears production totaled 47 million

tons and 17 million tons, respectively. World exports, on the other hand,

reached 5 million tons (apples) and 1.6 million tons (pears).

-

China leads the world production

of fresh pears and apples, accounting for over 50% of the total volume.

Additionally, it is the No. 1 fresh apple exporter, but only contributes

20% of the world supply, followed by Chile and Italy, which together

account for 30%.

-

Argentina only surpasses

China in world fresh pear exports, ranking first with 30% of supply.

This position has been earned by the regular supply of well-known

quality varieties enjoying good market acceptance, such as the Williams

and Packham’s Triumph pears.

-

Moreover, Argentina is the

major pear producer and exporter in the Southern Hemisphere.

-

The world demand for pome

fruit is led by Russia, which has become a major consumer in recent

years.

-

Apple and pear global import

and processing are mostly concentrated in the Northern Hemisphere,

while countries in the Southern Hemisphere play a more prominent role

as suppliers.

-

Thirty percent of the world

apple production goes to the processing industry, of which half is

in turn crushed to obtain juice concentrate.

-

Only 10% of the world pear

production is processed. Canned pears are the main by-product, followed

by juice concentrates.

-

With half the world volume,

China also leads the apple juice concentrate production and export,

while the USA and Argentina manufacture 90% of the pear juice concentrate.

-

These are 70° Brix concentrate

products (degrees Brix measure sugar concentration), which in the

case of apple juice are mainly used as sweeteners by carbonated soft

drink manufacturers. Pear juice, on the other hand, is mostly used

to manufacture juices for direct consumption.

DOMESTIC PRODUCTION

-

Argentina produces 1.8 million

tons of pome fruit, of which 60% corresponds to apples.

-

Between 1998 and 2007, the

domestic pear production increased by almost 40%, mainly due to technological

investment and new pear orchards. This scenario contrasts with the

sharp y-o-y fluctuations in apple production, which in some periods

exceed 20%.

-

The apple and pear growing

area is located in the Alto Valle (Upper Valley) of Río Negro

and Neuquén Province, and in the Valle Medio (Medium Valley)

of Río Negro Province, which concentrate 80% of production.

-

The remainder is grown in

the Uco Valley (Mendoza Province). Other less important areas include

25 de Mayo (La Pampa Province), and the Tulum Valley (San Juan Province).

-

It is estimated that there

are 27,175 hectares (67,150.88 acres) of apple and 22,028 ha (54,432.37

acres) of pear orchards.

-

Apple and pear growers (around

4,000) are associated in a Federación de Productores de Frutas

de Río Negro y Neuquén (Federation of Río Negro

and Neuquén Fruit Growers), while in Mendoza Province the most

representative organization is the Cámara de Comercio, Industria

y Agricultura de Tunuyán (Tunuyán Chamber of Commerce,

Industry, and Agriculture).

-

In the valley of Río

Negro and Neuquén and the middle valley, 50% of the farms have

a surface area of less than 10 ha (24.7 acres), while in Mendoza Province

farms of this kind represent 90%.

-

Sixty-five percent of the

domestic apple harvest corresponds to the Red Delicious variety and

clones; 15% corresponds to Gala and clones, with the same percentage

for Granny Smith. The remaining 5% is divided up among Pink Lady,

Rome Beauty, Golden Delicious, Fuji, and Braeburn varieties.

-

Although still in an initial

stage, a change of variety (especially through Gala) is under way

in view of the preferences in the global marketplace.

-

With regard to the pear varieties

grown, 45% of the total volume corresponds to Williams and 30% to

Packham’s Triumph. These are followed by Beurre D’Anjou

(10%), Red Bartlett (6%), and Abate Fetel (2%). The remaining percentage

includes Beurre Bosc, Beurre Giffard, Clapps Favourite and Red Beurre

D’Anjou.

-

The pear harvest starts at

the beginning of January and ends in mid-March, while the apple harvest

extends from late January through mid-April.

-

A tentative harvest schedule

is defined by the National Service of Agricultural Food Quality and

Health (SENASA as per its Spanish acronym) (Resolution SAG No. 554/83

and Resolution ex IASCAV No. 203/93), based on the optimal ripeness

of fruit, and it changes with each variety.

-

Growers and/or packers must

request permission at the local SENASA delegations prior to harvesting.

-

Fifty percent of growers

are independent and are only involved in the first sale stage of the

product. Those who are fairly integrated (i.e., they pack and market

their production) account for 30% of the total and have greater bargaining

power.

-

The remaining percentage

corresponds to fully integrated growers who, in addition to having

cutting-edge technology throughout the production chain, control exports.

Production Destination

(%)

| |

Export |

Industry |

Domestic Market |

| Apple |

22 |

50 |

28 |

| Pear |

63 |

25 |

12 |

-

The codling moth (Cydia

pomonella) or “apple and pear maggot” is the pest that

inflicts the most severe damage to these fruits and hence to the regional

economy. Apart from the direct losses caused by damaging the fruit,

the pest also limits access to new markets and to traditional destinations

such as Brazil, which has imposed quarantine restrictions.

-

The SENASA, jointly with

the Plant and Animal Health Commission of the FunBaPa (Patagonian

Zoo- and Phytosanitary Barrier Foundation, have developed a pest control

program aimed at reducing pest damage below a threshold level that

may ensure the competitiveness of fruit produced in the region for

trading purposes.

-

Mendoza Province, through

the Iscamen (Instituto de Sanidad y Calidad Agropecuaria, Farming

Health and Quality Institute), has a pest alert system in place.

-

Cultural practices account

for 50% of apple and pear growing costs, while harvesting accounts

for another 20%.

-

Owing to the type of variety

sold and the quality of fruit for fresh consumption, the markets for

these fruits are very different.

-

Pear production, favored

by the excellent quality of the Williams variety, mostly goes to fresh

consumption, and particularly to exports.

-

As to apple production, 50%

of the crop goes to the processing industry due to the scarce Argentine

supply of the varieties most demanded by international customers,

and to the high percentage of fruit failing to meet the fresh market

quality standards. Eighty percent of the processed volume is crushed

to obtain juice concentrate.

PACKING

- This process comprises the selection and

preparation of fruit prior to cold storage.

- This chain has around 300 packing plants,

40%of which are fitted with cold-storage rooms. A gradual concentration

of packing stations is observed, and the Cámara Argentina de

la Fruta Integrada (CAFI) (Argentine Integrated Fruit Production Association)

comprises the largest number of packing and cold storage facilities.

- Twenty-five percent of packing plants are

fully integrated to the chain (production-packing-cold storage-exports).

- The main reasons for fruit damage on packing

lines include metabolic changes, mechanical damage, and infestation

by pests and diseases. In most cases, containers are assembled, filled,

and sealed manually, using tape dispensers, stapling and strapping

devices.

- The most common containers for apple packing

are the Telescópico Mark IV (18.5 kg/40.78 lb. cardboard boxes)

for EU shipments, and the Torito Jaula (19-20 kg/41.88-44.09 lb. wooden

crates) for shipments to the domestic market.

- Fresh pear shipments to the EU are packed

in Standard Chileno (19 kg/41.88 lb.) crates, Telescópico 4/5

(20 kg/44.09 lb.) corrugated cardboard boxes, and Telescópico

Sudafricano (15.2 kg/33.51 lb.) corrugated cardboard boxes.

- Pear shipments for the domestic market use

the same packaging as apples.

- Demand for labor in packing operations is

high during harvesting, and is reduced by more than half after picking.

- Cold storage helps control the production

going to the packing facilities and enables crops to be sold out of

season at better prices.

- There are nearly 200 cold-storage facilities,

50% of which are fully integrated.

- The installed capacity averages 2.6 million

cubic meters (91.8 million cubic ft.).

- Containers and labor account for 60% of total

apple and pear packing costs, while cold storage accounts for another

25%.

- Most small growers choose a packing plant

for marketing their crops. At the primary stage, there are some cases

of vertical integration of co-ops and packing plants, which move forward

along the chain by processing production.

- Most purchase operations are done on a “per

kilogram of fruit delivered at the packing plant” basis, when

the price and terms of payment are arranged. Growers are usually paid

part of the amount agreed upon to cover harvesting costs.

- During the 2003 crop year, the Ley Provincial

Nº 3.611 de Transparencia Frutícola (Provincial Law No

3611 on Fruit Production Transparency) was enforced. The law provided

for a legally binding relationship regime applicable to the different

links in the production chain in Río Negro Province. This law

requires that all purchase agreements be formalized in writing and

provide data on the fruit, as well as the terms and conditions of

delivery, payment, grading, and culling. Growers and companies endorsing

this system shall benefit from a series of tax rebates.

PROCESSING

-

In the Alto Valle and Valle

Medio region, and in Mendoza Province, a network of agro-industries

has been set up for the manufacture of juice concentrate, cider, dehydrated

and canned fruit, dehydrated pulp, and liqueurs.

-

Juice concentrates are produced

by concentration of juice from several apple or pear varieties. Manufacture

takes place mostly from January through May.

-

Argentina’s production

of apple juice concentrate averages 60,000 tons, while pear concentrate

totals only 25,000 tons per crop season.

-

Variations in juice concentrate

production are a direct function of the availability of fruit for

crushing and of international juice prices.

-

The industry uses 6.7 kg

(14.77 lb.) of apples, on average, to obtain 1 kg (2.20 lb.) of juice

concentrate, while for pears, the ratio is 7.4 kg (16.31 lb.) to 1

kg (2.20 lb.).

-

There are two types of concentrates

– clear concentrate (70°-71° Brix) used in the juice

and carbonated drink industry, and cloudy concentrate (60° Brix)

for making juices and nectars.

-

The product is stored in

307 kg (676.81 lb.) plastic or metal drums or, most often, in wooden

bins with a net capacity of 1,535 kg (3384 lb.). In both cases, the

juice is kept in a polyethylene bag.

-

There are 10 juice concentrate

manufacturers, mainly SMEs, operating 11 industrial plants, most of

which are members of the Cámara Argentina de la Industria y

Exportación de Jugos de Manzana, Peras y Afines - CINEX (Argentine

Apple and Pear Juice and Related Products Export and Industry Association),

headquartered in Cipolletti (Rio Negro Province).

-

The installed capacity is

approximately 100 thousand tons, which due to the seasonal nature

of production is idle most part of the year.

-

The juice sector provides

employment to 1,000-1,100 skilled workers.

-

In the last decade, the investment

of fruit juice companies was focused on process streamlining. The

technology used is of Italian and American origin.

-

Fruit is the factor with

the strongest incidence on juice concentrate production costs, followed

by enzymes (imported from Germany and France), and packaging.

-

Apple and pear essences are

by-products recovered during the concentration of apple and pear juice,

and they are sold separately. They represent between 0.5% and 1% of

juice concentrate production and are used by the beverage and perfume

industries.

-

Another by-product obtained

is dehydrated fruit of excellent quality that satisfies the most demanding

markets.

-

Dehydrated apples and pears

are sold in a variety of presentations (small dice, slices, dice with

peel, wedges, segments, dice without additives, and powder), and are

vacuum-packed in bags of 10 kg (22.04 lb.), 12.50 kg (27.55 lb.),

or 22.68 kg (50 lb.), which are in turn placed in cardboard boxes.

-

The product has a variety

of uses – confectionery, breakfast cereals, snacks, food services,

and dairy industry, among others. There are 2 companies manufacturing

1,400 tons of dehydrated apples per year, obtained from the Granny

Smith and Red Delicious varieties. On the other hand, less than 1,000

tons of dehydrated pears are produced per year, mainly made from the

Williams variety.

-

Cider is another apple by-product,

and the Argentine Food Code allows an addition of up to 10% of pear

juice concentrate to the end product.

-

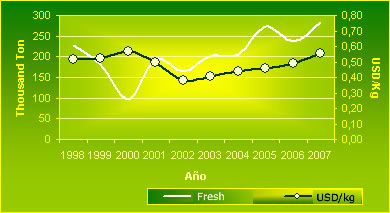

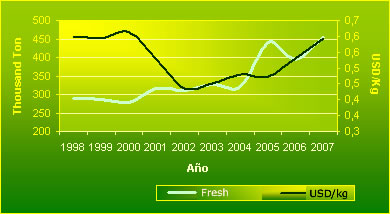

In 2007, Argentina exported

283,000 tons of fresh apples and 454,000 tons of fresh pears, which

represented USD156 and USD269 million in foreign currency inflow,

respectively.

-

In the period 1998-2007,

fresh pear exports were the largest growth category (60%), showing

an uptrend, just like apple exports, which increased by 25%.

-

Russia, a member of the CIS

(Commonwealth of Independent States), and Brazil concentrate nearly

50% of Argentine fresh apple and pear exports. However, as far as

regional trade blocs go, the main destination is the European Union,

with 35% and 40% of the total supply, respectively.

|

-

The categories exported

are “premium”, “choice”, and “commercial”

grades (Resolution SAG No 554/83).

-

Six exporters sell 50%

of the total volume. Some are fully integrated, right to the shelves,

as a result of their partnering with foreign companies that own

retail chains in the European Union.

-

Most fruit shipments to

overseas destinations (Russia, the European Union, and the US) are

exported through the ports of San Antonio Este (SAE), in Rio Negro

Province, and Buenos Aires, while land shipments to Brazil are made

through Santo Tomé (Corrientes Province) and Bernardo de

Irigoyen (Misiones Province).

-

SAE is a port specializing

in fruit shipments due to its closeness to the growing areas (450

km/281 miles).

-

From March through June,

fruit is shipped to the European Union, with most cargo being handled

in the first two months. During the second half of the year, there

are more exports to Brazil. This sale pattern serves to offset labor

seasonality.

-

The Rotterdam and Hamburg

markets are the gateways to the European Union; in Brazil, fruit

is sold through the Sao Paulo and Porto Alegre wholesale markets.

-

During the 2002-2003 crop

year, a Risk Mitigation System (RMS) was implemented for all fresh

apple and pear exports to Brazil. This scheme consists in sampling

on-farm and at packing, as well as registry and inspection of final

pack. Plant health officials from both countries participate and

the aim is to certify the absence of live Carpocapsa (codling moth)

larvae.

-

Ninety-five percent of the

Argentine apple and pear juice concentrate production is exported,

basically to the USA, thus supplying more than 30% of the American

market demand for clear juice concentrate. Philadelphia is the port

of entry.

-

As is the case with the fresh

category, processed exports are made through the Port of San Antonio

Este.

-

Two companies account for

70% of total exports, while the first four account for 90% of shipments.

From December through January, some exporters gather to arrange the

chartering of vessels. However, no association has been set up to

sell the product.

-

In addition to the traceability

requirements, HACCP, and good manufacturing practices (GMP) already

imposed by the USA, the Bioterrorism Act was enforced in December

2004.

-

The increase in global supply

(especially as a result of China’s soaring growth as a producer

and exporter) poses further challenges for Argentina in terms of quality

requirements and the need to find new ways of cutting down costs.

-

The USA imports 70% of Argentina’s

dehydrated apple production, and together with the United Kingdom

and Chile, accounts for 65% of Argentine dehydrated pear exports.

-

Only 3% of canned pears go

to the global market, with the USA being the main buyer.

-

Fruit for the domestic

and Brazilian markets is shipped by land. In the first case, reefers

or temperature-controlled trucks are used for transporting 1,000

boxes each, equivalent to 20 pallets. In some cases, trucks are

used that are not fitted with temperature control systems; these

are covered with tarpaulins, sometimes insulated, which could

result in impaired fruit quality.

| |

Common

Mercosur

Nomenclature

(NCM) |

Common

External

Tariff |

Extra-zone

Import

Duties |

Intra-zone

Import

Duties |

Export

Duties |

Export

Drawbacks |

| Frash Apple |

0808.10.00 |

10 |

10 |

0 |

10 |

3,40 |

| Dehydrated Apple |

0813.30.00 |

10 |

10 |

0 |

5 |

5,00 |

| Apple Juice Concentrated |

2009.71.00 |

14 |

14 |

0 |

5 |

5,00 |

| Fresh Pear |

0808.20.10 |

10 |

10 |

0 |

10 |

2,70 |

| Dehydrated Pear |

0813.40.10 |

10 |

10 |

0 |

5 |

5,00 |

| Canned Pear |

2008.40.10 |

10 |

10 |

0 |

5 |

4,05 |

| Pear Juice Concentrated |

2009.80.00 |

14 |

14 |

0 |

5 |

5,00 |

..Source:

National Food Administration based on AFIP. |

-

Shipments to Brazilian market

destinations are adequately refrigerated. Vehicles have greater capacity

as they can load 1,200 boxes (22.8 tons). Freight services in the

Mercosur bloc are largely outsourced, with a majority of Brazilian

carriers.

-

Fruit exported to the European

Union and the USA is shipped through different maritime transportation

services, such as TEU 20’ containers with a capacity of 10 pallets,

or FEU 40’ containers with a capacity of 20 pallets.

-

A standard cargo hold is

mostly used for transporting fruit in pallets.

-

Juice concentrate is transported

on reefers at 0°C (32 °F) for clear juice concentrate, and

at -20 °C (-4 °F) for cloudy juice.

-

The dehydrated product is

transported in standard cargo holds at room temperature, by ship or

truck depending on the country of destination.

-

As from March 2002, the EU

is implementing FAO ISPM–15 (ISMP - International Standards

for Phytosanitary Measures), which rule on the treatment required

for wood packaging material including dunnage used in international

trade.

-

Pursuant to Resolution 626/03,

the Secretariat of Agriculture, Livestock, Fishing and Foods (SAGPyA

as per its Spanish acronym) has created the Registro Nacional de Centros

de Aplicación de Tratamientos a Embalajes de Madera (CATEM)

(National Registry of Wood Packaging Material Treatment Centers),

which are authorized by the SENASA to apply the heat or fumigation

treatments recommended by ISPM-15.

The table above illustrates the tariffs (in %) imposed on pear and

pear by-product exports:

-

On average, Argentina consumes

8 kg (17.63 lb.) of fresh apples and 3 kg (6.61 lb.) of fresh pears

per inhabitant, per year, which is rather low as compared to China

and the European Union. In Argentina, national consumption promotion

campaigns are still infrequent.

-

Eighty percent of the apples

consumed in the domestic market correspond to the Red Delicious variety,

11% to the Granny Smith, and 6% to the Gala type. Argentine consumers’

favorite pear is the Williams (60%), with the Packham’s Triumph

accounting for 35%.

-

Barely 25% of the domestic

supply is sold through the Buenos Aires Central Market. Although this

channel is becoming less relevant, it is still seen as a price benchmark.

-

In recent years, other markets

in the provinces, such as Córdoba, Mendoza, Tucumán,

and Rosario, have gained importance.

-

A major change has taken

place in the apple and pear domestic distribution with the expansion

of direct sales to supermarkets and hypermarkets, the upgrading of

green grocers, and greater diversity in demand. In addition, retail

distributors are applying more stringent requirements regarding quality,

health, color, and size.

-

The Central Market receives

fresh apples and pears all year round, with 50% of the total volume

being concentrated from February to June, while apple distribution

is more evenly spread. In both cases, there is a supply shortfall

between November and January.

-

A marked price seasonality

is observed – prices plunge to their lowest level in April,

coincidentally with larger volumes arriving at the Buenos Aires Central

Market, and then rise until their peak in November and December.

-

The most common grades for

domestic consumption are the “choice” and “commercial”

varieties.

-

Despite the technological

developments, there is still inadequate management and an over handling

of goods from the harvest stage down to the shelves.

-

The National Food Administration

runs courses for retailers and wholesalers, basically on fruit and

vegetable post-harvest handling. Also, the importance of customer

service is highlighted, taking into account that consumers are becoming

increasingly knowledgeable and well -informed.

CONSULTED SOURCES

AFIP - CASTRO, A. R. 1998. Análisis

de la Cadena Agroindustrial de Fruta de Pepita. Documento Nº

1. Unidad de Información y Estudios Económicos, EEA

Alto Valle - CAFI (Cámara Argentina de Fruticultores Integrados)

- Cámara de Comercio, Industria y Agricultura de Tunuyán

- CINEX (Cámara Argentina de la Industria y Exportación

de Jugos de Manzanas, Peras y Afines) - CHEFTEL, J, 1992. - Introducción

a la Bioquímica y Tecnología de los Alimentos - DEHAIS,

F., consultor privado, com. personal - Dirección de Fruticultura

de Neuquén - Federación de Productores de Fruta de

Río Negro y Neuquén - Fundación IDR (Instituto

de Desarrollo Rural de Mendoza) - Secretaría de Fruticultura

de Río Negro - IERAL, Fundación Mediterránea

– INTA, EEA Alto Valle, 1999.- Fruticultura Moderna, Proyecto

de Cooperación Técnica INTA-GTZ - JORGE, J., com.

personal - RODRIGUEZ DE TAPATTA, A. Fruticultura de Exportación,

Pomáceas y Cítricos Dulces, Secretaría de Política

Económica - www.mecon.gov.ar

- www.fas.usda.gov - www.funbapa.org.ar

(Fundación Barrera Zoofitosanitaria Patagónica) -

www.patagonia-norte.com.ar

(Puerto San Antonio Este) - www.senasa.gov.ar

- www.sinavimo.gov.ar (Sistema

Nacional Argentino de Vigilancia y Monitoreo de Plagas) - www.afip.gov.ar.

|